The Capital Allocator's Trap

The Capital Allocator’s Trap

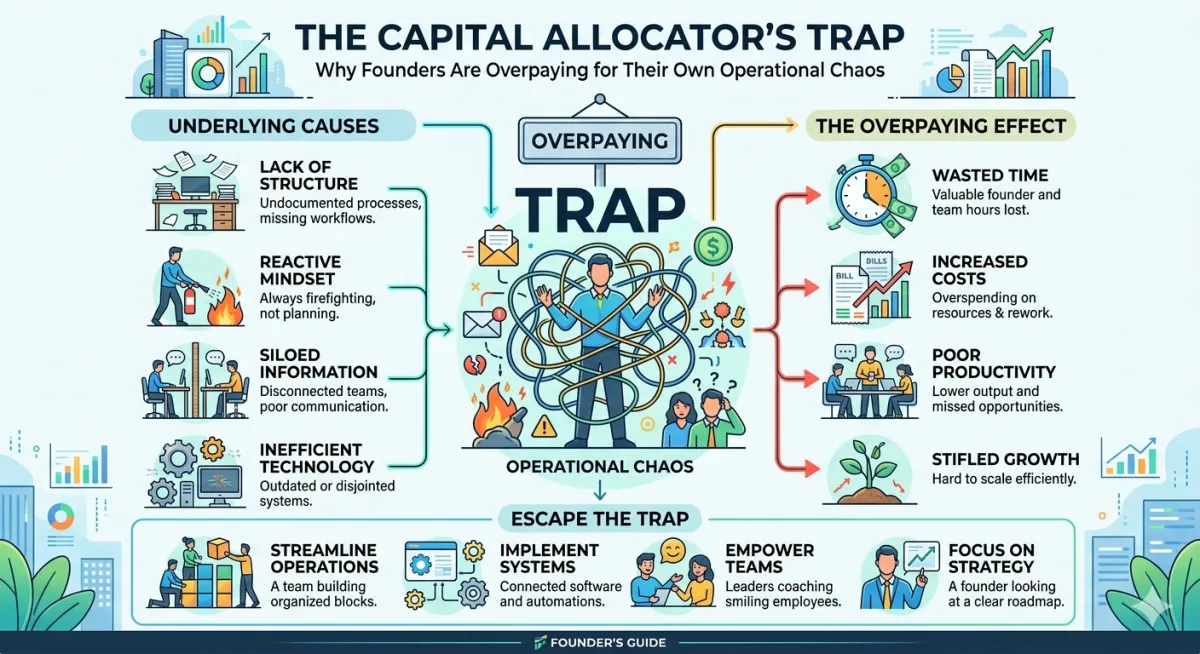

Why Founders Are Overpaying for Their Own Operational Chaos

If public companies managed capital the way many privately owned businesses manage operations, shareholders would revolt.

Investors would not tolerate unclear reporting lines, decision bottlenecks that run through a single executive, or high-cost labor routinely performing low-value tasks. They would not accept growth funded by managerial exhaustion. They would demand structural fixes.

Yet inside founder-led companies, this pattern is remarkably common.

Owners often see themselves as builders, operators, or product visionaries. In reality, once payroll begins and capital is committed, the job description quietly changes. The founder becomes the firm’s primary capital allocator. Time, talent, and cash must be deployed toward the highest-return activities available.

Many companies fail at this not because the leadership lacks intelligence or effort, but because they misprice the internal cost of operational disorder.

They treat chaos as a management inconvenience when it is, in fact, a capital allocation failure.

The Hidden Cost of Organizational Friction

Financial statements rarely show inefficiency explicitly.

A profit-and-loss statement lists payroll, rent, software subscriptions, and marketing spend. It does not show the hours lost reconciling data between systems, chasing approvals through Slack threads, or manually transferring information across tools that should communicate automatically.

These activities accumulate into what could be called organizational friction.

Friction behaves economically like a tax.

Employees spend time coordinating work rather than producing it. Managers devote attention to resolving exceptions rather than designing better systems. Founders intervene to resolve routine problems that should have been addressed structurally.

The costs are real even if they are difficult to isolate.

Labor economists have long observed that productivity depends less on individual effort than on how effectively organizations coordinate complex work. In the United States, nonfarm labor productivity rose about 2.3 percent in 2024, according to the Bureau of Labor Statistics, yet unit labor costs still increased roughly 2.6 percent. In other words, output improved but labor remained expensive. Businesses that deploy labor inefficiently feel that pressure quickly.

For smaller firms, the consequences can be amplified.

When systems are weak, organizations compensate with people. Hiring becomes the default solution to operational problems that are fundamentally structural.

That approach works temporarily. It rarely scales.

How Businesses Became Operationally Fragmented

The roots of the problem lie partly in how companies adopted technology over the past two decades.

Most firms did not design integrated operating systems. They accumulated tools.

Accounting software solved one problem. CRM platforms solved another. Project management tools, marketing automation systems, payroll platforms, and internal messaging apps followed. Each department optimized locally.

The result was a technology stack built incrementally rather than architecturally.

Information now moves through many businesses in awkward, manual ways. Data is copied across systems. Teams rely on ad hoc spreadsheets to reconcile differences. Managers coordinate through meetings and chat threads rather than through structured workflows.

In effect, the founder often becomes the integration layer.

The model works while the organization is small. But as complexity grows, the founder’s attention becomes a bottleneck. Decision velocity slows. Errors multiply. Reporting becomes opaque.

This is not unusual.

Research from McKinsey indicates that while a majority of companies report using artificial intelligence in at least one function, only a minority have redesigned core workflows around these tools. Many firms are adding technology on top of already fragmented systems rather than rebuilding processes from the ground up.

The result is more capability without necessarily more coherence.

The Real Economics of Automation

Much of the current enthusiasm around artificial intelligence focuses on its potential to replace labor.

The more interesting economic effect is often different.

AI systems frequently function as coordination technologies. They reduce the need for human effort in routine transfer work: routing information, summarizing documents, categorizing requests, and standardizing responses.

In a widely cited study examining more than 5,000 customer support agents, researchers from Stanford and MIT found that access to generative AI increased productivity by roughly 14 percent. The largest gains occurred among less experienced workers, whose performance moved closer to that of top performers.

The implication is subtle but important.

AI did not primarily create genius-level productivity. It reduced variance and standardized competence.

A separate experiment conducted by Harvard Business School and Boston Consulting Group found similar patterns. Consultants using AI completed more tasks and finished them faster on problems within the system’s capabilities. But on tasks outside those capabilities, users relying on AI performed worse.

The lesson is clear: automation works best where work is structured, repeatable, and measurable.

Where judgment, ambiguity, or creative reasoning dominate, technology becomes an assistive tool rather than a replacement.

This distinction matters because many companies pursue automation backwards. They attempt to apply AI to strategic work while leaving routine operational coordination unchanged.

From a capital allocation perspective, that is exactly the wrong order.

Why Founders Continue to Overpay for Chaos

If operational inefficiency is so costly, why does it persist?

Part of the answer is psychological.

Hiring someone to fix a problem feels faster than redesigning a process. Replacing broken workflows requires confronting uncomfortable questions about organizational structure, accountability, and leadership discipline.

There is also a visibility bias.

Payroll appears clearly on financial statements. Process inefficiency does not. Owners see the cost of employees but often underestimate the cost of misdirected labor.

Finally, founder-led companies often reward responsiveness rather than structural thinking. Solving a problem immediately feels productive. Building systems that prevent the problem from recurring requires patience.

Over time, this produces a subtle but powerful pattern.

Human labor becomes the flexible glue holding together fragmented operations.

That glue is expensive.

The Capital Allocation Consequences

Operational chaos has effects that extend beyond daily inconvenience.

First, it distorts profitability. When highly compensated employees perform routine coordination work, labor costs rise without corresponding increases in output.

Second, it concentrates risk. Businesses where information flows through the founder or a small group of senior operators become vulnerable to disruption if those individuals step away.

Third, it slows decision-making. Opportunities that require rapid action can be missed when basic reporting and coordination processes are inefficient.

Finally, and most importantly for owners, it traps wealth inside the business.

Companies burdened by operational friction often generate less distributable cash than their revenues suggest. Owners reinvest earnings into hiring and short-term fixes rather than building financial security outside the firm.

The business becomes the owner’s entire balance sheet.

That concentration risk can be severe.

Entrepreneurs often assume their company is their greatest asset. In reality, it may also be their least diversified one.

Where the AI Narrative Goes Wrong

The current excitement around AI sometimes obscures these underlying structural issues.

Technology alone rarely solves operational dysfunction. In fact, poorly implemented automation can amplify problems by accelerating flawed processes.

Industry analysts warn that a significant share of AI initiatives fail to move beyond pilot programs. Gartner has projected that roughly 30 percent of generative AI projects may be abandoned after proof-of-concept stages due to poor data quality, weak governance, or unclear economic value.

This is not surprising.

Automation requires disciplined process design and reliable data infrastructure. Without those foundations, even sophisticated technology produces inconsistent results.

The organizations capturing meaningful returns from AI are typically those that begin with workflow redesign rather than tool adoption.

They treat automation as an operational engineering exercise, not a technology experiment.

A More Useful Framework for Business Owners

For founders seeking to improve capital efficiency, the question is not simply whether to adopt AI.

The more relevant question is how to redeploy human attention toward work that genuinely requires human judgment.

A practical approach involves several steps.

First, distinguish between judgment work and transfer work. Judgment work involves decision-making, negotiation, creativity, and problem-solving. Transfer work involves routing information, formatting documents, reconciling records, and tracking tasks.

Second, measure how often the founder must intervene in routine operations. High founder involvement often indicates structural weaknesses rather than leadership strength.

Third, identify processes with high frequency, high coordination costs, and significant error consequences. These are prime candidates for workflow redesign and automation.

Finally, treat operational improvements as capital investments. Evaluate them using the same rigor applied to equipment purchases or acquisitions: expected cost reductions, productivity gains, and payback periods.

This discipline reframes automation from a fashionable technology initiative into a straightforward economic decision.

The Real Endgame: Optionality

The ultimate objective of operational efficiency is not simply higher margins.

It is optionality.

Companies that generate consistent surplus cash flow give their owners choices. Earnings can be distributed, diversified into other assets, invested in new ventures, or reserved for downturns.

In contrast, businesses trapped in operational complexity often require continuous reinvestment simply to maintain stability.

Owners may appear successful on paper while remaining financially exposed to a single enterprise.

From a capital allocator’s perspective, that is an uncomfortable position.

The purpose of building a business is not merely to create activity. It is to create durable financial flexibility.

That outcome depends less on revenue growth than on the quality of the underlying operating system.

A business that runs efficiently without constant intervention behaves like an asset.

One that depends on perpetual managerial heroics behaves more like a job.

Strategic Implications

For operators, the immediate priority should be diagnosing where human effort is compensating for weak processes.

For investors evaluating founder-led companies, operational discipline deserves as much scrutiny as financial performance. Businesses that rely heavily on key individuals often carry hidden fragility.

For executives managing larger organizations, the next phase of AI adoption will likely be less about experimentation and more about structural redesign. Companies that reengineer workflows will capture disproportionate gains.

Those that simply add tools may see little change.

The Real Question

Every founder should occasionally ask a simple question:

If this business were an investment opportunity in the public markets, would I accept this level of operational opacity, labor inefficiency, and key-person risk?

Many owners discover the answer is no.

That realization is uncomfortable. It is also useful.

Because once the problem is framed correctly—as a capital allocation issue rather than an operational annoyance—the solution becomes clearer.

The work of building a business does not end with revenue growth.

It ends when the enterprise operates with enough structural discipline to generate wealth without consuming the owner in the process.

Contrarian Discussion Questions

Are most founders actually under-investing in systems because labor has historically been too cheap?

Does AI primarily create productivity gains, or does it simply expose how poorly many organizations were designed?

Are investors systematically overvaluing founder-led businesses that depend heavily on individual operators?

Could the next wave of competitive advantage come less from technology itself and more from organizational architecture?

Are entrepreneurs too focused on building businesses when they should be focused on building balance sheets?